.avif)

.avif)

Every world‑changing technology begins as a paper in a peer‑reviewed journal, but only a fraction ever becomes a product someone can buy. Deep tech ventures—those that commercialize quantum processors, iron‑air batteries, CRISPR editors, or meta‑materials—must build a market even as they finish the science, a juggling act few software founders ever attempt. The challenge is compounded by the infamous “Valley of Death,” the funding gap between laboratory proof and commercial traction. A deliberately crafted go‑to‑market (GTM) plan therefore belongs at the very first white‑board session, maturing in parallel with technology, manufacturing, regulatory, and financing roadmaps.

When these readiness staircases rise in lock‑step, risk is revealed early and capital is deployed precisely where it clears the next obstacle. What follows below is a step‑by‑step guide—each piece building on the last—that shows how scientists can transform a brilliant experiment into a bankable enterprise. Follow along, and the journey becomes a deliberate climb—no leaps of faith required.

Capital Strategy: Layering Dilutive and Non‑Dilutive Funding

The climb begins with money, yet traditional venture checks rarely cover the marathon between prototype and factory ramp. Savvy founders orchestrate a blend of non‑dilutive grants, flexible government contracts, and mission‑driven corporate venture capital so that each tranche unlocks a clearly defined milestone. In the United States, the SBIR/STTR program now offers up to $2.4 million across Phase I and II, while Defense Innovation Unit (DIU) OTAs shorten the path from demonstration to purchase order (Defense Innovation Unit, 2025).

That surge of government momentum is drawing in corporate venture capital as well: Lockheed Martin Ventures has enlarged its investment fund and added new hardware bets, while DCVC Climate joined several Series B rounds in 2024 to accelerate climate‑scale infrastructure (DCVC, 2024). These investors gravitate toward plans that echo the Defense Innovation Board’s “five‑to‑ten capabilities in 36 months” guideline, because such plans tie capital gates to measurable risk reduction (Defense Innovation Board, 2024). Finally, founders who publish transparent use‑of‑funds—how much for pilot lines, how much for quality systems—signal fiscal discipline that accelerates term‑sheet negotiations. With funding secured, the company is now positioned to identify its target customer base.

Market Discovery & Segmentation

Capital without customers is philanthropy, so the next leap is from hypothesis to validated demand. Teams start by interviewing every potential stakeholder and mapping pains with the Jobs‑to‑Be‑Done lens, which converts a novel algorithm or catalyst into outcomes executives can understand. Studies show JTBD‑oriented start‑ups reach problem–solution fit nearly a quarter faster than feature‑first peers (Hobcraft, 2024). These interviews surface not just users but veto players—regulators, procurement officers, insurers—whose objections can kill a sale long before procurement. By clustering prospects according to workflow, regulatory burden, and budget authority, founders isolate a “beachhead” market willing to pay for immediate relief rather than distant potential. The discovery output then feeds persona‑specific collateral: engineers receive spec sheets, financial buyers receive ROI models, and risk managers receive compliance matrices. Continuous feedback loops keep the map accurate as technical capabilities evolve, ensuring the next dollar and development sprint are aimed at a target that will pay. With problem–solution fit charted, attention shifts to the factory floor.

Manufacturing & Supply‑Chain Readiness

A prototype that dazzles on the bench can still implode on the assembly line, which is why investors watch Manufacturing Readiness Level (MRL) as closely as Technology Readiness Level (TRL). The DoD MRL Deskbook lays out ten rungs from lab tool to rate production (Department of Defense, 2022). Form Energy’s decision to break ground on a West Virginia gigafactory while still running 150‑MWh pilots shows how pairing TRL 7 with MRL 5 earns both market credibility and $405 million in follow‑up capital (Associated Press, 2024). Likewise, PsiQuantum’s partnership with GlobalFoundries lets it piggyback on a mature photonics supply chain rather than building one from scratch. Founders should present an MRL glide‑path that includes supplier audits, statistical‑process‑control targets, and ISO 9001 certification dates, thereby de‑risking scale‑up for skeptical customers. As tooling is ordered and quality systems harden, regulatory clocks begin to tick—making foresight in compliance the next critical staircase.

Regulatory & Standards Planning

Time‑to‑revenue is often gated by regulators, not engineers, so founders must weave compliance milestones into every Gantt chart. In therapeutics, the U.S. FDA’s exploratory‑IND pathway permits micro‑dosing studies that generate human data months earlier than traditional routes (Food & Drug Administration, 2005). In materials, looming EPA PFAS bans and EU REACH revisions can upend bills of materials, forcing painful redesigns. Effective teams engage regulators early, scheduling pre‑submission meetings before design freeze and aligning toxicology studies with pilot production. They also track standards consortia—ISO 4210 for batteries, IEEE 2861 for quantum‑safe encryption—because future procurement specs often embed these norms. Integrating regulatory tasks with engineering sprints prevents the expensive purgatory that doomed high‑profile ventures like Theranos, where sales promises outran validation (Carreyrou, 2018). Once compliance paths are credible, deep‑tech start‑ups can court their most demanding first customer: government.

Government‑as‑First‑Customer & Dual‑Use Pathways

Defense and security agencies crave frontier technology yet tolerate risk differently than commercial buyers. MIT’s Dual‑Use Readiness Levels™ framework helps founders sequence SBIRs, OTAs, and production contracts so that mission pull accelerates—not derails—commercial objectives (Keselman & Murray, 2024). DIU’s Blue UAS 2025 refresh proves the model: 23 new drones won accreditation after a three‑day fly‑off, opening immediate sales to U.S. agencies and, by extension, critical‑infrastructure operators (Defense Innovation Unit, 2025). Nevertheless, defense revenue can become a cul‑de‑sac if a company fails to articulate how lessons learned in uniform translate to logistics, energy, or agriculture. Founders should therefore frame mission contracts as proving grounds that harden the product and shorten later enterprise sales cycles. When executed well, government credentials offer early revenue, technical validation, and a reputational halo that lowers barriers in adjacent markets. With credibility established, the company must now communicate value to a broader audience.

Positioning & Messaging

Deep‑tech marketing is part storytelling, part specification. Audiences range from PhD engineers to CFOs, each demanding a tailored narrative that links input to impact. Form Energy’s phrase “multi‑day storage at grid‑relevant cost” instantly maps iron‑air chemistry to a utility’s balancing problem, exemplifying outcome‑driven messaging. Crafting a message hierarchy—executive elevator pitch, technical white paper, risk‑manager FAQ—lets every stakeholder find his or her level of detail without diluting technical credibility. Third‑party endorsements such as DOE grants, NATO DIANA selections, or peer‑reviewed data provide social proof that overcomes early‑adopter hesitancy. Consistent tone—confident yet sober—differentiates deep‑tech ventures from hype‑heavy consumer apps, protecting brand equity in sectors where failed pilots linger in memory. A well‑tuned narrative then arms the sales team to engage enterprise accounts with precision.

Sales Motion & Ecosystem Integration

Enterprise buyers rarely “click to subscribe” on hardware. Most require a narrowly scoped, paid pilot that de‑risks performance and integration before multiyear commitments. Anduril mastered this “land, integrate, expand” playbook, co‑funding its Ghost Shark factory in Australia to satisfy sovereignty needs and opening Indo‑Pacific channels in the process. Where success hinges on complementary assets—hydrogen pipelines for fuel cells, cryogenic plants for quantum—start‑ups can sweet‑talk partners by offering integration toolkits or revenue sharing. Clear pilot metrics, cybersecurity approvals, and post‑pilot pricing tiers should be codified in the initial statement of work to prevent proof‑of‑concept limbo. Meanwhile, channel partnerships with OEMs leverage existing sales engines without ballooning internal headcount, yet still provide feedback loops critical to product iteration. As deployments scale, the company must scale its people as rigorously as its servers or reactors.

Talent & Organizational Design

Great hardware is built by interdisciplinary teams, not lone geniuses. Yet most spin‑outs begin with academics fluent in physics but not in quality systems or enterprise sales. Europe’s Next Generation Innovation Talents program embeds graduate engineers and product managers into deep‑tech SMEs for six‑month rotations, offering a replicable model for cross‑functional upskilling (European Innovation Council, 2024). Internally, milestone‑based incentives align curiosity with commercialization, while rotating scientists into customer‑facing roles breeds empathy for operational constraints. Advisory boards stacked with ex‑regulators, supply‑chain veterans, and Fortune 500 buyers fill experience gaps until full‑time hires are justified. Talent dashboards that track skills against roadmap needs reveal gaps before they stall a launch. In short, culture must evolve as quickly as code if the company is to survive the transition from lab notebook to production line.

Intellectual Property & Freedom‑to‑Operate

Intellectual‑property strategy is the moat that protects all other investments. Layering claims—composition, process, and application—makes design‑arounds prohibitively costly, while international filings secure future manufacturing and sales territories. Freedom‑to‑operate analyses must precede enterprise pilots because indemnity clauses push infringement risk onto vendors. Trade‑secret regimes and cyber‑security certifications add alternative layers when patents are impractical or export‑controlled. Annual portfolio reviews keep coverage aligned with evolving product features and competitor activity. Investors increasingly ask for quantitative IP scorecards—time‑to‑grant, citation velocity, geographic breadth—so proactive reporting reassures them that the moat is widening, not eroding.

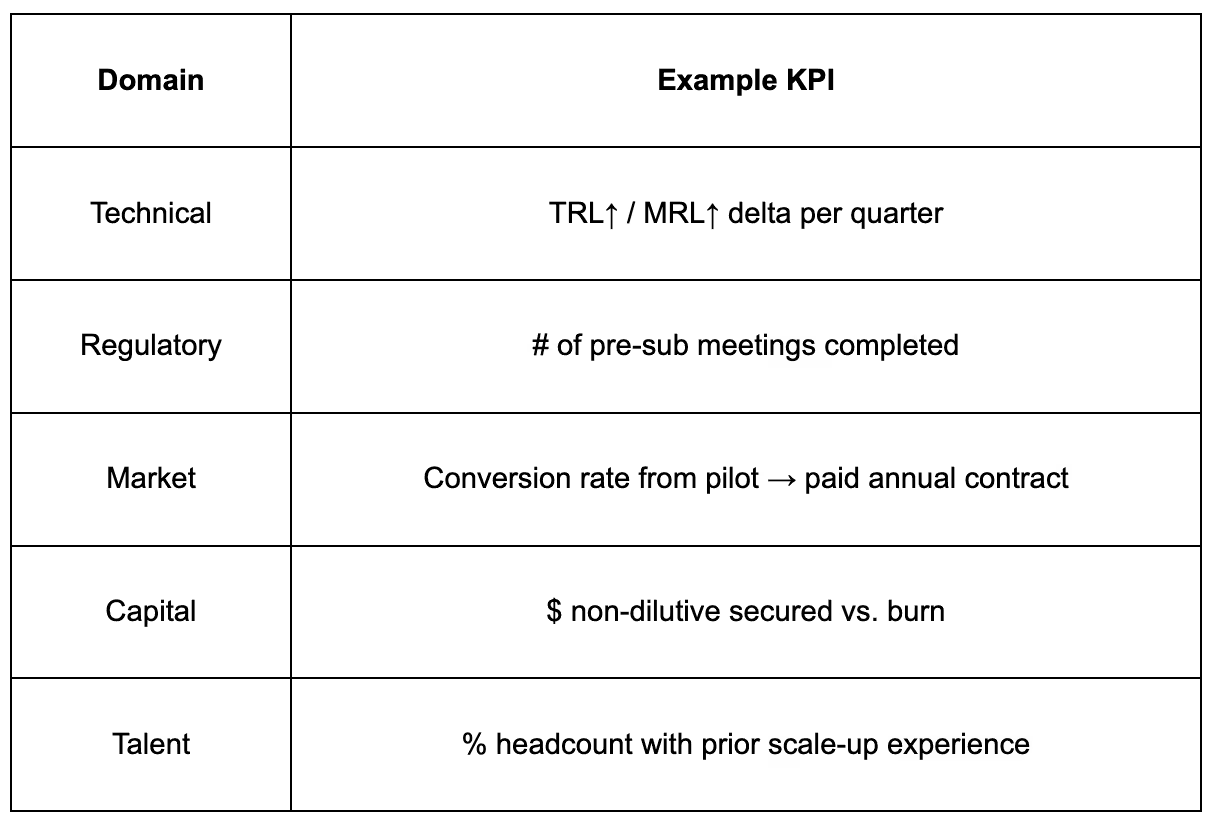

Metrics That Matter

In deep tech, audited revenue may not arrive for years, yet boards need proof of momentum today. Leading indicators bridge the gap. Tracking quarterly TRL and MRL deltas quantifies technical and manufacturing velocity; logging regulatory pre‑submission meetings shows compliance progress. Pilot‑to‑contract conversion rates reveal market traction, while the ratio of non‑dilutive funds to burn highlights capital efficiency. Finally, the percentage of staff with prior scale‑up experience gauges organizational readiness. Publishing these metrics—warts and all—in investor updates sustains trust and surfaces bottlenecks early, allowing corrective action before value evaporates.

Case Studies in GTM Execution

Form Energy synchronized factory construction with signed utility PPAs, attracting $405 million to accelerate 100‑hour storage batteries (Associated Press, 2024). Anduril leveraged defense OTAs and a sovereign co‑manufacturing venture to validate its autonomous systems, then expanded into Indo‑Pacific defense markets. PsiQuantum opted for strategic patience, partnering with GlobalFoundries and securing $25 million in U.S. Air Force funds to prepare a photonics fab for fault‑tolerant qubits (PsiQuantum, 2023). Each example underscores how aligning one staircase—manufacturing, procurement, or capital—with the others turns a risky leap into a measured step.

Conclusion & the Readiness Staircase

Commercializing deep‑tech innovations is less a moonshot than a Himalayan ascent: every camp must be stocked, every rope anchored, and every climber acclimatized. By treating GTM as integral to product architecture—assigning owners, gates, and metrics to the staircases of technology, manufacturing, regulation, market, and capital—founders convert the valley of death into a series of manageable landings. The “Readiness Staircase” visualization, stacking TRL, MRL, regulatory stage, and GTM milestones on a single axis, reminds teams that skipping even one step invites a fatal fall. With this blueprint, researchers can move beyond the lab—transforming from visionary dreamers into disciplined innovators, prepared to reshape industries and bolster national resilience.

.avif)

References

Anduril Australia. (2024, August 15). Anduril Australia to build Ghost Shark factory. https://www.anduril.com/article/anduril-australia-to-build-ghost-shark-factory/

Associated Press. (2024, October 31). Climate solution: Form Energy secures $405 million to speed development of long‑awaited 100‑hour battery. https://apnews.com/article/climate-battery-energy-storage-iron-822f329c8a4f7518f4db6b24d6fcd15c

Carreyrou, J. (2018). Bad blood: Secrets and lies in a Silicon Valley start‑up. Knopf.

DCVC. (2024). Deep Tech Opportunities Report 2024. https://www.dcvc.com/reports/deep-tech-opportunities-report-2024

Defense Innovation Board. (2024). Aligning incentives to drive faster tech adoption. https://innovation.defense.gov/Portals/63/20240701%20DIB%20Report_Aligning%20Incentives%20PUBLISHED%20STUDY_1.pdf

Defense Innovation Unit. (2025, February 14). Blue UAS refresh list, framework platforms and capabilities selected. https://www.diu.mil/latest/blue-uas-refresh-list-and-framework-platforms-and-capabilities-selected

Department of Defense. (2022). Manufacturing Readiness Level (MRL) deskbook (Version 2022). https://www.dodmrl.com/MRL_Deskbook_2022__20221001_Final.pdf

European Innovation Council. (2024). InnoNext: The Next Generation Innovation Talents initiative. https://eic.ec.europa.eu/

Food & Drug Administration. (2005). Guidance for industry: Exploratory IND studies. https://www.fda.gov/media/72325/download

Keselman, G., & Murray, F. (2024). Introducing Dual‑Use Readiness Levels™: A framework for dual‑use strategy (MIT Working Paper). https://dualuse.mit.edu/wp-content/uploads/2024/11/Dual-Use-Readiness-Levels.pdf

PsiQuantum. (2023, May 23). U.S. Government to provide $25 million to a GlobalFoundries/PsiQuantum partnership. https://www.psiquantum.com/news-import/schumer-announces-25-million-for-globalfoundries-and-psiquantum-to-develop-the-next-generation-of-quantum-computers-at-rome-air-force-research-lab-amp-malta-campus

.avif)

.avif)

.avif)

.avif)